The Circle Jensen Drew

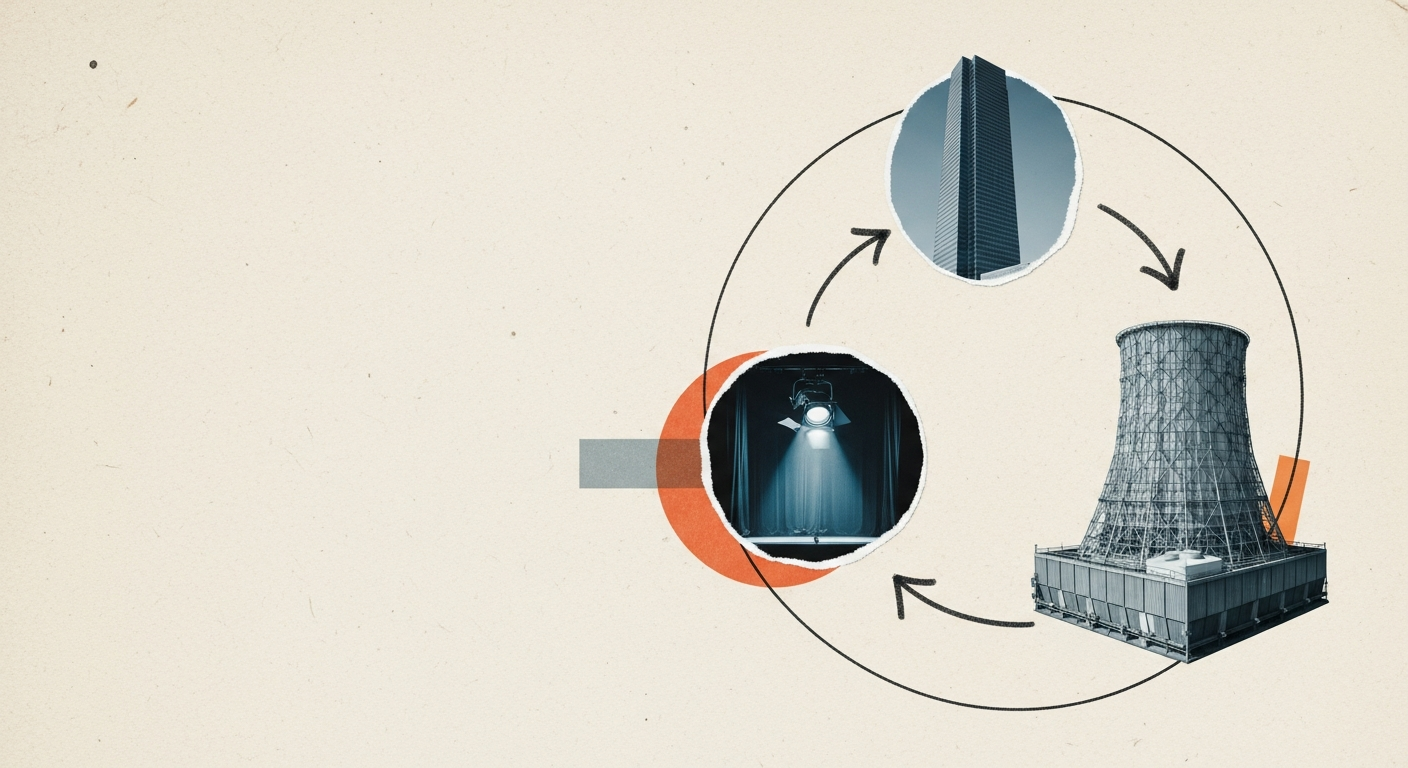

NVIDIA put $2bn of equity into CoreWeave; CoreWeave disclosed a $27bn Meta deal, $12bn earmarked for Vera Rubin. The capital is moving in a circle.

NVIDIA put $2 billion of equity into CoreWeave at $87.20 a share this week. On the same stage at GTC 2026, CoreWeave disclosed a $27 billion infrastructure deal with Meta, $12 billion of which is earmarked for Vera Rubin capacity, the next-generation NVIDIA platform. Jensen Huang called it "the largest infrastructure buildout in human history," which is the sort of thing Jensen says on most Tuesdays, but in this case the accountants will back him up.

I want to write about what this transaction actually is, because the headline version ("NVIDIA invests in cloud partner") and the cynical version ("circular financing propping up the bubble") are both too thin, and neither one tells you what to watch.

Here is the shape of it. NVIDIA sells GPUs to CoreWeave. CoreWeave borrows against those GPUs to buy more GPUs from NVIDIA. NVIDIA takes an equity stake in CoreWeave, partially financing CoreWeave's ability to keep buying GPUs from NVIDIA. Meta signs a $27 billion contract with CoreWeave to rent those GPUs, and roughly half of that contract value is in effect pre-committed to NVIDIA's next platform generation. Meta is simultaneously buying NVIDIA silicon directly for its own data centres. The same dollars circulate through the same three parties in at least two directions, and when Jensen stands on stage and announces the arrangement, NVIDIA's market cap moves enough to more than fund the equity stake he just committed.

NVIDIA takes an equity stake in CoreWeave, partially financing CoreWeave's ability to keep buying GPUs from NVIDIA.

This is the anatomy. The question is whether it's pathology.

The circular-financing frame and its limits

The bear case writes itself, and several people have written it. Dot-com-era telcos did something that rhymes: Lucent lent money to CLECs so the CLECs could buy switching gear from Lucent. Nortel did the same. Cisco did the same, on a smaller scale. When the CLECs couldn't service the debt, the vendors booked the write-downs and the stocks collapsed. The circularity was the tell. Revenue that depends on your customer's ability to raise capital against the assets you just sold them is not revenue in the way a textbook would recognise it.

There is something to this, and I don't want to wave it away. If you drew the cash flows on a whiteboard you would find loops, and loops of this shape did blow up an industry twenty-five years ago. The question is whether the analogy holds on the specifics that matter, and my honest answer is: partially, in a way that should worry NVIDIA shareholders less than it worries CoreWeave shareholders, and should worry CoreWeave shareholders less than they're currently pricing in.

Three differences from the Lucent comparison are load-bearing.

First, the end demand. Lucent's CLECs were selling telecom capacity to a market that turned out not to exist at the prices the business plans assumed. Bandwidth was a commodity, marginal cost was falling toward zero, and the customers the CLECs needed never showed up. CoreWeave's end customer, in this specific deal, is Meta, a company that generated roughly $165 billion of revenue last year, spent north of $40 billion on capex, and whose willingness to write cheques for compute is constrained by its belief that Llama-scale training runs and agent-scale inference are worth the money. You can argue Meta is wrong about that. You cannot argue Meta is a shell. The $27 billion contract is backed by one of the eight or nine balance sheets on Earth large enough to make it mean something.

Second, the asset. A Lucent switch in 2001 had a useful life measured in a decade or more, but its resale value collapsed because the protocols were moving and the installed base was shrinking. An H100 in 2024 had a useful life closer to three to five years in frontier training and perhaps seven in inference, but its resale market is deep and the queue for replacement parts runs months long. GPUs depreciate quickly but they also clear. Blackwell and Rubin will make Hopper-generation cards cheaper, not worthless. The securitisable value of CoreWeave's fleet is not what NVIDIA's pricing suggests, but it is not zero and it is not close to zero.

Third, and this is the one people miss, the vendor's position. Lucent needed the CLECs because Lucent's direct enterprise and incumbent-telco business was mature and slow-growing; vendor financing was how it juiced its numbers. NVIDIA does not need CoreWeave in that sense. NVIDIA's direct hyperscaler demand, Microsoft, Google, Amazon, Meta buying silicon to stuff into their own data centres, exceeds supply. The $2 billion into CoreWeave is not demand creation. It is demand shaping: steering a particular slice of capacity toward a particular set of customers (mid-market AI labs, enterprise workloads, Meta's burst capacity) that NVIDIA wants served without having to run the colo business itself.

So the Lucent analogy gives you the shape of the risk but miscalibrates the magnitude. This is not a vendor inventing its customers. It is a vendor with real customers choosing to equity-fund a specific distribution channel because the channel has strategic value beyond the revenue it generates.

That said, and I want to be careful here, because it's the bit the bulls skip, the reason NVIDIA is writing the equity cheque rather than just selling more cards is precisely that CoreWeave's capital structure can't quite carry what NVIDIA wants it to carry without help. CoreWeave's debt load is, by any ordinary standard, extraordinary. Its revenue is concentrated in a small number of customers. Its margin on GPU leasing depreciates faster than its debt amortises. The equity injection at $87.20 is a vote of confidence, but it's also a capital subsidy, and capital subsidies exist because the market wouldn't fund the next expansion at terms NVIDIA considered acceptable. That is worth saying out loud.

What NVIDIA is actually buying

If you strip the equity stake down to its economic function, NVIDIA is doing three things at once and the $2 billion is cheap for any one of them.

It is buying option value on an independent neocloud tier. The hyperscalers, Microsoft, Google, AWS, are both NVIDIA's largest customers and its largest strategic threats. Each of them is building custom silicon (Trainium, TPU, Maia) that aims, over a horizon of years, to displace NVIDIA in their own workloads. NVIDIA's response has been to invest in an independent layer, CoreWeave, Lambda, Crusoe, a handful of others, that will remain NVIDIA-first because it has nothing else to sell. If Microsoft's Maia works and Azure starts training its frontier models on it, NVIDIA wants a CoreWeave-shaped alternative already at scale for every AI lab and enterprise that still wants the NVIDIA stack. $2 billion to underwrite that insurance is a rounding error on NVIDIA's cash position.

It is buying distribution for the CUDA platform. The cards are the tip; the moat is the software. CoreWeave is not just renting GPUs, it is renting a full NVIDIA stack, CUDA, NIM microservices, NeMo, the whole platform catalogue. Every workload that runs on CoreWeave is a workload with switching costs to anything else. NVIDIA's platform strategy requires that there be places to run NVIDIA platforms that aren't owned by companies building competing platforms. The equity stake aligns CoreWeave with that software roadmap in a way a supply contract cannot.

It is buying a marketing asset. The Meta $27 billion announcement is worth more to NVIDIA's narrative than the margin on the underlying silicon. Every number Jensen puts on a GTC slide, "the largest infrastructure buildout in human history," "$3-4 trillion of AI infrastructure by 2030", requires proof points. Meta signing a $27 billion contract at GTC 2026, with $12 billion of Vera Rubin pre-commitment, is a proof point. It tells every enterprise board member watching that the forward demand curve is real, that the next-generation platform has buyers already, and that sitting out is expensive. NVIDIA could not have bought that signal in any other way for $2 billion.

The cleanest way to price this: NVIDIA's market cap moved by something in the order of a hundred billion dollars on the week of GTC. If even a single-digit percentage of that move is attributable to the CoreWeave/Meta announcement rather than to the Rubin roadmap itself, the equity stake has paid for itself twenty times over on the day it was committed. This is the arithmetic Jensen is working with. It is not complicated.

What Meta is actually buying

The Meta side of the transaction gets less attention and deserves more. Meta spent $40 billion-plus on capex last year and is guiding higher. It is building its own data centres at pace, training Llama at frontier scale, and has been publicly willing to commit to open-weight release of its models. It does not, on the face of it, need CoreWeave.

The $27 billion makes sense for two reasons. First, latency of capacity. Meta's own data-centre buildouts take two to four years from site acquisition to productive GPU hours. Renting from CoreWeave in the interim, at a premium to self-build, but available now, lets Meta pull forward its training roadmap by twelve to eighteen months. In a world where the competitive half-life of a frontier model is months rather than years, paying rent to move faster is the correct trade.

Second, optionality on model generation. The $12 billion Vera Rubin commitment is not Meta saying "we want Rubin in 2027." It is Meta saying "we want first access to Rubin when it ships, at a price we've locked in now, against capacity we don't have to build." Rubin's successor after that is already in NVIDIA's roadmap. Meta is buying the right to keep pace without having to bet its own construction timeline against NVIDIA's silicon timeline. CoreWeave absorbs the timing risk. Meta pays a premium for it. That premium is CoreWeave's entire business model.

This, incidentally, is why the circular-financing frame misses the point. The $27 billion isn't NVIDIA buying demand for its own silicon through a proxy. It's Meta paying CoreWeave to bear the construction-timing risk that Meta doesn't want on its own balance sheet. NVIDIA benefits, but NVIDIA isn't manufacturing the demand. The demand exists because frontier AI training requires capacity faster than any single company can build it, and Meta would rather rent than wait.

Where I part company with the bulls

I've defended the transaction on its economic logic, but there are two things the bull case tends to skip over, and I want to put them on the table.

The first is that CoreWeave's equity is pricing a version of the future where GPU leasing remains a high-margin business for a decade or more. I am not convinced that's right. The neocloud tier, CoreWeave, Lambda, Crusoe, and a long tail behind them, is in the process of commoditising itself. There are no durable technical moats in renting GPUs. CUDA is NVIDIA's moat, not CoreWeave's. Scale is a real advantage but it's an advantage the hyperscalers have more of. The end state of this market, absent some structural intervention, is a set of thin-margin capacity providers competing on price and utilisation, with NVIDIA capturing the bulk of the economic surplus and the neoclouds getting whatever is left after depreciation and interest.

The equity investment changes this calculus for CoreWeave specifically, which is the point. By aligning with NVIDIA at the cap-table level, CoreWeave gets preferential allocation of scarce silicon, co-marketing, architectural input, and a hedge against commoditisation that its pure-play competitors don't have. This is why Lambda and Crusoe are, in their own ways, chasing similar arrangements. The neocloud tier is sorting itself into NVIDIA-aligned and not-NVIDIA-aligned, and the aligned ones will eat the unaligned ones. This is rational. It is also, for CoreWeave shareholders, a story about being the chosen vassal, not about being a principal. Vassals do well in good years. They do not become kings.

The second thing the bulls skip is the correlation structure of the risks. The case for CoreWeave's debt load and Meta's willingness to pay and NVIDIA's forward demand curve all rest on the same underlying bet: that AI training and inference demand continues to grow at something like the current trajectory for the next three to five years. If that bet is right, everything in this transaction works. If that bet is wrong, if model capability plateaus, or if inference economics force a restructuring of how compute is priced, or if one of the major labs shows that you can get frontier performance with an order of magnitude less compute, then the entire chain unwinds at once.

This is the part that should keep CoreWeave shareholders awake. Their equity is a leveraged, correlated bet on a single scenario. The $2 billion from NVIDIA does not diversify that bet; it concentrates it. If the AI capex cycle slows, CoreWeave's revenue, Meta's willingness to pay, NVIDIA's stock price, and the value of CoreWeave's GPU fleet all move in the same direction at the same time. The bear case isn't that any one of these fails. The bear case is that they fail together, and the capital structure has no room to absorb even a mild synchronised downturn.

I don't think that downturn is the base case. I do think the equity is priced as though it couldn't happen, and things that can't happen sometimes do.

What to watch

Four things, in roughly increasing order of importance.

Utilisation rates on the CoreWeave fleet. GPU leasing businesses live or die on utilisation. Any quarter where CoreWeave's utilisation drops below the mid-eighties tells you the supply-demand balance is tilting. The Meta contract provides a floor under this for the next several years, but the marginal card, the card not committed to Meta or to another anchor tenant, is where the market signal lives.

The Vera Rubin launch schedule. $12 billion of the Meta contract is Rubin-specific. If Rubin ships on time and performs as advertised, the contract looks cheap in retrospect. If Rubin slips by six months or disappoints on efficiency gains, the pre-commitment looks expensive and the whole structure of forward-booked capacity starts to wobble. NVIDIA has historically executed these launches well. The question is whether that continues under the pressure of current volumes.

Hyperscaler custom silicon adoption curves. If Microsoft's Maia, Google's TPU v6, and AWS's Trainium 3 start taking meaningful share of their own internal workloads in 2026-2027, the thesis that "the independent neocloud tier is strategically essential to NVIDIA" strengthens, and CoreWeave becomes more valuable to NVIDIA over time, not less. If the custom silicon disappoints and the hyperscalers quietly go back to buying more NVIDIA, CoreWeave's strategic insurance value declines. This is counter-intuitive: CoreWeave benefits from NVIDIA being threatened.

The next equity round. If NVIDIA is still writing equity cheques to CoreWeave in twelve months, it means CoreWeave's independent access to capital remains constrained, which means the market is pricing in more risk than NVIDIA is. If NVIDIA does not need to write another cheque, it means CoreWeave has graduated to a standalone capital structure, which is the outcome NVIDIA actually wants. The absence of a follow-on round is the bullish signal. The presence of one is the bearish signal, dressed up as a vote of confidence.

The shape of it

I started by saying neither the headline version nor the cynical version of this transaction tells you what to watch. Here is where I've landed.

This is not circular financing in the Lucent sense. The end demand is real, the customers have balance sheets, the asset has residual value, and the vendor isn't manufacturing its own revenue. It is, however, capital subsidy in aid of strategic architecture: NVIDIA is using its cash position to shape the neocloud tier into a form that serves NVIDIA's long-run interests, and the neoclouds that align with it will do better than the ones that don't.

The risk is not fraud. The risk is correlation. Everyone in this chain is making the same bet, and the bet is roughly correct, and the equity prices assume it is more than correct, that it cannot meaningfully fail. The history of infrastructure buildouts is that they are always more or less correct on direction and catastrophically wrong on pace and scale at the equity level. Railways got built. Railway shareholders got wiped out twice before the railways paid. Fibre got laid. Fibre shareholders got wiped out. The AI infrastructure buildout is probably more of the same, and the question isn't whether it happens, it's happening, but whether the equity holders who financed it get paid before the next wave of equity holders dilutes them.

Jensen drew a circle at GTC 2026. The circle is real. Real circles can still be too tightly drawn. I would be long NVIDIA on the logic above, cautious on CoreWeave at current multiples, and attentive to anything that looks like a synchronised move in the four signals above. When the circle tightens, it tightens all at once.

Footnotes

Discussion

No comments yet, be the first.